Retirement

It's an odd thing to consider your retirement as your career is only beginning. However, experts agree that it's vital to start saving for retirement as soon as possible. Financial security in retirement takes planning and commitment, but the good news is that it can be easier than you think. The idea behind saving early for retirement is that your money can grow at a higher average rate per year than the average inflation rate and you will be in a much stronger position to maintain the type of lifestyle you want even after you are no longer working.

Individual Retirement Accounts (IRAs)

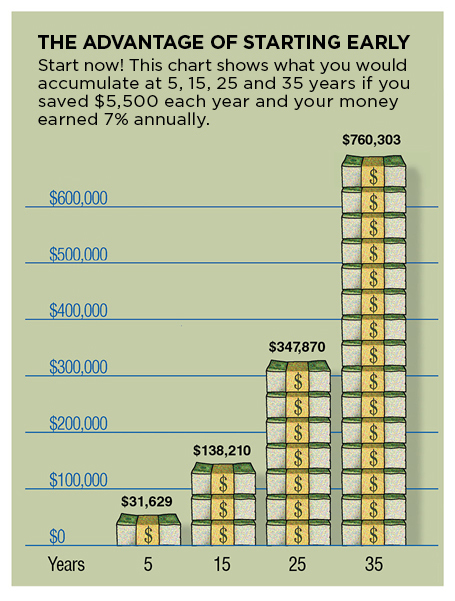

You can start an Individual Retirement Account (IRA) at any time. You can contribute $5,500 each year to the account – more after you turn 50. The United States Department of Labor shares this chart showing how a $5,500 annual savings can add up over the years:

Source: United States Department of Labor

The individual contributions to your retirement account have already been taxed. The benefit of contributing taxed funds is that when you withdraw funds after retirement from an IRA the funds are not taxed!

Other types of retirement savings accounts

401(K) and 403(b)

A 401(k) account is a retirement savings account facilitated through your employer. A 403(b) is a similar retirement savings account offered if your employer is a non-profit or if you have qualified self-employment.

Many employers offer retirement savings matches. Since this match is essentially free money, you should take full advantage! Since contributions to a 401(k) and a 403(b) are pre-tax deposits through payroll deductions, it may be a simple way for you to save since the money won't be readily available to you.

However, you cannot access this money without penalty until you reach retirement. When you do withdraw funds after retirement, the funds will be taxed.

Pension plans

Pension plans are also offered through your employer. Pension plans offer you a specific amount of income on retirement and are guaranteed for your lifetime. Pension plans are not as popular as they once were, but should your employer offer one, you will want to inquire about your ability to participate in the plan.