Loans

There are a variety of reasons you might choose to pursue a loan in your lifetime. Every day consumers turn to loan options to help them finance their education, purchase a car or purchase their first home. We talk a lot about student loans when discussing financial wellness, so a good starting point is to take a step back to understand some of the key concepts and terms associated with loans in general. There are a lot of things you need to understand before you sign the dotted line. We've outlined some of them here to help you get started.

Principal

The principal is the total sum of money borrowed and any interest that has been capitalized.

Interest rate

Interest is money charged by and paid to the lender in exchange for borrowing money. Interest is calculated as a percentage of the unpaid principal amount (loan amount) borrowed. The interest rate may be determined by a calculation determined by the lender, most often depending on your credit score and other factors used in assessing risk such as your debt-to-income ratio. The interest rates on federal student loan programs are set by Congress.

There are two primary types of interest rates: fixed and variable. Fixed interest rates are very straightforward: the interest rate remains the same for the life of the loan. Variable interest rates, however, can change with the financial markets or based on other factors, which can impact your payment amount.

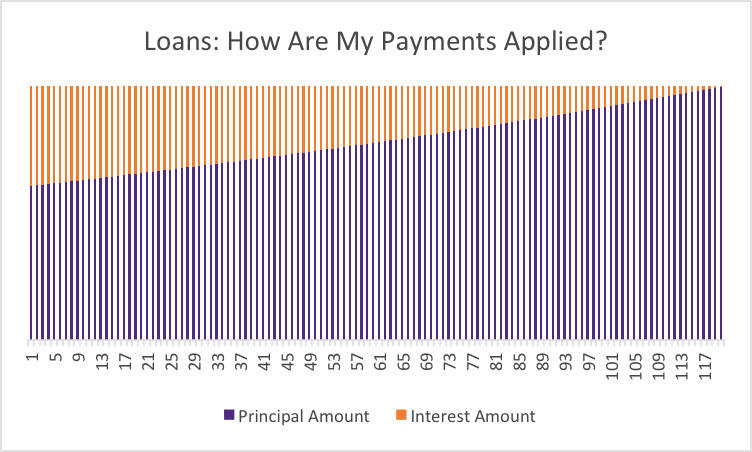

With either type of interest rate, each loan payment you make will generally first apply toward any late fees, then toward the interest accrued since your last payment, then toward the principal. This means that, over the life of a loan, your earlier payments will mostly just cover the interest that accrues. As you pay down the principal, your loan will accrue less interest, and your later payments will cover more principal.

This is an example of a $10,000 loan with a 5% interest rate and a repayment term of 10 years (120 monthly payments). As demonstrated, you can see that more of the initial payments are applied toward the interest.

Capitalization

Interest capitalization occurs when the unpaid accrued interest is added to the principal balance of the loan. After capitalization, you are now being charged interest on a higher principal amount, essentially your interest can begin to accrue interest.

If you make more than the minimum payment due on your loan, the “extra” amount you put toward the loan may be applied toward the principal (consult your lender for details). Paying down the principal early means that you will pay off your loan faster and ultimately pay less interest in the long term.

Repayment terms

Repayment terms will vary by loan. Components of loan terms will include length of time to repay the loan and minimum payments. It is important to understand the basic terms to ensure you meet your obligations.

Some loans, like car loans, commonly offer a basic repayment plan. For example: You borrow a $25,000 auto loan at a fixed interest rate of 3.11% to be repaid over a 60-month period. You will begin repayment the month after you purchase the vehicle. The monthly payment is $450, and the total amount you will pay is $27,026. In addition to the principal amount of $25,000, the cost of the loan is $2,026.

Federal Student Loans offer several different repayment plans. It's important to consider the long term impact of your choice, and remember that you can increase your payment at any time.

Contract/promissory note

The loan contract is a legally binding document. This document will outline the terms and conditions of the loan, interest rate, fees and all of your rights and responsibilities as a borrower. This protects both you and the lender by documenting the agreed upon terms.

It should go without saying, but it is extremely important to take the time to read this information carefully. While many are long and can feel overwhelming, the “fine print” includes all the important details of your contract; if you don't read or understand it fully, it can cause immense stress down the road. Ask for help if you don't feel like you understand the contract. Don't assume you know what's in the contract; while many will contain terms and conditions that you expect, others may have surprising requirements or details.

Security vs. unsecured

A secured loan is a loan that requires collateral. The contract will stipulate that if the loan goes unpaid, the lender can seize the collateral in order to protect or avoid forfeiting their investment. One common example is an auto loan; if the borrower defaults on the loan, the lender will repossess the vehicle. Home loans and other large item purchases like a boat or motorcycle are usually purchased with secured loans.

Loans can also be “unsecured,” meaning that they have no collateral tied to the contract. If an unsecured loan goes unpaid, the lender can take legal action against the borrower, but there is no collateral to retrieve. Typically, student loans and personal loans are unsecured. Failing to repay unsecured loans can still lead to serious consequences, such as a significantly negative impact on your credit, garnished wages and future ability to borrow.

Other considerations

- Ask if an auto-debit discount is available. Some lenders offer discounts or rate reductions to borrowers for having setting up their payments to be debited automatically from their bank account.

- Some contracts will increase your interest rate if you make one late payment, or require you to repay the entire loan on demand if you miss one payment.

- Find out if your loan has a prepayment penalty. Some lenders will charge a fee if you pay off your loan early.

See Consumer Financial Protection Bureau: Compare Loan Offers and explore interest rates for more information.